FIRST, SOME BACKGROUND

FIRST, SOME BACKGROUND

First things first, you’ll need a Self-Managed Super Fund (SMSF) if you want to buy an investment property with your super savings. Borrowing money can have several benefits for people with an SMSF which make it well worth considering. However, you need to be careful because there are also risks whenever you borrow money to invest as loses will be magnified.

To examine the benefits, we will begin by looking at the background of the Limited Recourse Borrowing Arrangements (LRBAs) which are available for use by the SMSFs when investing in assets, and specifically when investing in residential or commercial real estate.

LIMITED RECOURSE BORROWING ARRANGEMENTS (LRBA)

The Superannuation Industry (Supervision) Act generally does not permit borrowing. However, since September 2007, SMSF Trustees are permitted to borrow money to spend on specific investment assets. In July 2010, the Act was amended to clarify how this exemption works. A further clarification was issued in 2012, specifying the terms of both borrowing for repairs and improvements, and the type of assets for which the borrowed money could be used.

An SMSF is permitted to borrow funds to purchase assets subject to these conditions:

1) Beneficial ownership

The asset acquired by the SMSF must be held in a Trust, with the SMSF being the holder of the beneficial interest in that asset. This means that the legal owner registered on the title deeds will be what is known as a ‘bare trust’ or a ‘custody trust.’ These requirements can complicate the acquisition of assets for an SMSF and it is crucial, therefore, that all the necessary required steps are taken before committing to this form of investment strategy. Professional financial advice is required.

2) Legal ownership

It must be understood that the beneficial owner of assets is the Trustee of the SMSF. Once the SMSF has this beneficial interest it then has the right to assume legal ownership of the asset, providing all borrowing used for the purchase has been fully repaid.

3) Single acquirable asset

An SMSF may borrow funds to acquire either a single asset (such as a residential property), or a group of identical assets of the same value which will be parceled together and regarded as a single asset. These assets must fulfill the conditions of the type of assets allowable for these types of funds.

For example, buying 1,000 shares in a single company would count as a single asset, but buying 500 shares in one company and 500 in another would not.

4) Limited recourse rights of the lender on default

Should the SMSF not keep up repayments on monies borrowed, the only asset which the lender can reclaim is the one for which these monies were specifically lent, i.e. no other assets or undertakings belonging to the SMSF may be claimed by the lender.

To cover against possible losses (for example, should the value of an acquired property fall below the sum borrowed) it is common for lenders to request a personal guarantee from Trustees as private individuals; in the event of a shortfall should the SMSF default on the loan, the Trustees may be liable as guarantors.

5) Restrictions on improvements

Funds cannot be borrowed for the purpose of making improvements to an asset held by the SMSF, this includes renovations on an investment property. The ATO made this clear in its ruling, Self-Managed Superannuation Funds Ruling SMSFR 2012/1.

It is important to distinguish between repairs and improvements.

For example, if a property suffers fire damage the SMSF Trustee may borrow funds for restoration or replacement of damaged items or building materials as this would come under the heading of ‘repairs’. However, borrowing to upgrade a property by building an extension, or by installing new bathroom or kitchen appliances, counts as an improvement and is not permitted.

6) Restriction on replacement assets

In certain limited situations, one acquired asset may be replaced by another, but only if it is of a similar nature to the original asset.

An example might be that a three-bedroom house is destroyed by fire: The SMSF could then build another more modern three-bedroom house to replace the asset. However, using the borrowed funds to build a larger property, or more properties on the same plot, would not be permitted.

TYPES OF PROPERTY YOU CAN INVEST IN

The types of assets which an SMSF is permitted to acquire using borrowed money must come within the allowable types of asset, under the Act, which may be acquired through direct investment. Permissible assets include:

- houses,

- residential units, and

- commercial property (office units, industrial warehouses, retail units etc).

It is not permitted for an SMSF to deliberately acquire an asset from any party which has an interest in the fund. This means that you can’t have your SMSF buy your existing investment property. You can’t even buy a property that is currently owned by a family member.

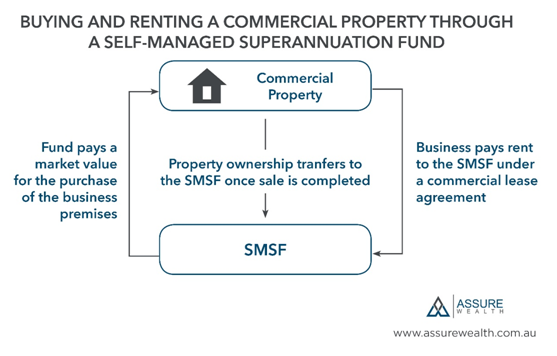

Business real property may be acquired providing market value is paid, however in some states there are Stamp Duty exemptions for this type of acquisition (e.g. Section 62A, NSW Stamp Duties Act). Business real property is defined as property which is used solely for the purposes of business (or several businesses). It is not compulsory for this to be your own business, but it is permissible, which makes it an attractive acquisition for those involved in running a business.

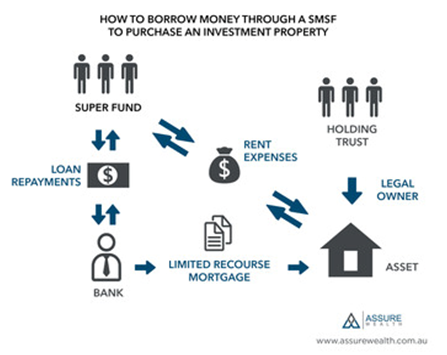

IMPORTANT: THE RIGHT BORROWING STRUCTURE

We can see here a common type of borrowing structure used for LRBAs:

Source: Assure Wealth

BORROWING MONEY TO BUY THE PROPERTY

Bank/Third-party lending

There are specific loan packages for SMSFs available from banks as well as several specialist lenders. These are specifically designed to comply with the various rules surrounding SMSFs.

There can be wide discrepancies between the terms and conditions offered by different lenders and you should take care when doing your research. I highly recommended that you partner with an expert Finance/Mortgage Broker with proven experience in SMSF lending.

The major banks no longer lend to SMSFs. However, there are a number of non-bank lenders who can lend up to 70% of the value of the property. You need to ensure you have an adequate cash buffer in your SMSF bank account to allow for costs and vacancies. Plus, you will need to be aware that an SMSF loan attracts higher fees and a higher interest rate than a standard investment loan.

A FINAL WORD

Using your super to buy an investment property can be a complex task, and there are serious consequences for getting it wrong. It’s very important to seek advice from a Financial Adviser who has specific SMSF qualifications and skills.

In part 2 of this series, we will show you the step-by-step process to go through to use your super to buy an investment property.

If this article interested you and you would like to speak to Pat Casey on the phone, select a time to speak Pat – Financial Planner Sydney.

At Assure Wealth we specialise in helping busy, successful families structure their finances to achieve greater wealth and financial peace of mind.

Author: Pat Casey – Managing Director & Financial Planner Sydney – Assure Wealth

Download the Assure Wealth Corporate Brochure

Disclaimer: The information provided on this website has been provided as general advice only. Assure Wealth does not provide direct property advice. We have not considered your financial circumstances, needs or objectives and you should seek the assistance of your Walker Lane Pty Ltd Adviser before you make any decision regarding any products mentioned in this communication. Whilst all care has been taken in the preparation of this material, no warranty is given in respect of the information provided and accordingly neither Walker Lane nor its related entities, employees or agents shall be liable on any ground whatsoever with respect to decisions or actions taken as a result of you acting upon such information.

Assure Wealth Pty Ltd ABN 31 965 466 780 Corporate Authorised Representative no. 1244817, Patrick Casey Sub-Authorised Representative no. 1244748 of Walker Lane Pty Ltd ABN 70 626 199 826, an AFSL holder No 509305.