Australia’s superannuation industry is the backbone of the country’s retirement system. It is the fourth-largest private retirement/pension fund market in the world, and is still growing. Self-managed superannuation funds (SMSF) currently make up 22.7% of total superannuation assets across nearly 600,000 funds.

The Different Types of Superannuation Funds

There are about 500 superannuation funds operating in Australia. Of those, 362 have assets totalling greater than $50 million. Superannuation assets totalled over $2 trillion at the end of the March 2015 quarter.

There are seven main types of superannuation funds:

- Industry Funds: funds generally run by unions or associations. Unlike Retail/Wholesale funds they are run for the benefit of members, as there are no shareholders. These funds are generally attractive to people who have low engagement with their superannuation as there are limited investment options and insurance arrangements that are subject to change by the Trustee.

- Wholesale Master Trusts: funds run by financial institutions such as banks. These are also classified as ‘retail funds’ by APRA.

- Retail Master Trusts/Wrap: funds run by financial institutions such as banks for individuals.

- Employer Funds: funds established by employers for their employees. Each fund has its own trust structure that is not necessarily shared by other employers.

- Self-Managed Superannuation Funds: are funds established for a small number of individuals (up to 4) and regulated by the Australian Taxation Office. Generally, the Trustees of the fund are the fund members (where there is a Corporate Trustee, the members are the directors of that company). SMSF property investment has gained considerable momentum since the amendment of borrowing provisions to allow for the purchase of residential real estate. The ability to obtain a limited recourse loan to buy an investment property in a low tax environment, has increased the popularity of property investment within SMSFs in recent times.

- Small APRA Funds (SAFs) are funds established for a small number of individuals (fewer than 5) but unlike SMSFs the Trustee is an Approved Trustee, not the member/s, and the funds are regulated by APRA. This structure is often used for members who want control of their superannuation investments but are unable or unwilling to meet the requirements to be a Trustee of a SMSF.

- Public Sector Funds are funds established by governments for their employees.

What exactly is a Self-Managed Superannuation Fund (SMSF)?

An SMSF is a structure that is set up by up to four individuals, with those same individuals acting as the trustees of the SMSF or directors if the SMSF has a corporate trustee. The purpose of an SMSF is to accumulate savings for retirement, and then pay pension payments to the members in retirement.

Due to the fact that the members of the SMSF are also the trustees, they have a lot of control over the running of the fund; the final word always lies with them even if they bring in outside help to consult in the more complex intricacies of managing an SMSF.

It is this level of control that has made SMSFs quite popular with a large number of Australians looking to secure their retirement future.

4 Reasons to Set up a Self-Managed Super Fund Today

1. Control – you steer the ship

As a trustee of an SMSF, you have all the control, not some faceless superannuation executive who is making decisions with your money. Not only does the trustee make decisions that directly impact the investment direction that fund takes, they also decide how much risk the fund is exposed to, plus is in charge of distributing payments such as pensions and death benefits.

The trustees choose exactly where they would like to invest the money, and they can always make changes when they feel it’s appropriate. This control gives the trustees and members of the super fund a much greater visibility and control over their investments. They have the power and ability to track their overall super balance, and have full autonomy over their investment decisions.

Having direct control in the management of the SMSF also gives members and trustees more interest in the superannuation, and subsequently their level of engagement increases. Though the trustees can hire outside help to consult on the more complex matters of running the self-managed super fund, the accountability ultimately lies in Trustee’s hands when it comes to the final decision.

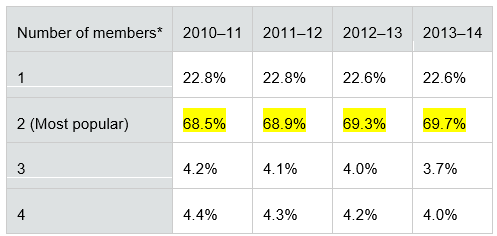

Number of Members per SMSF

*Source: ATO

2. Flexibility – change plans as needed

The flexibility with investment decisions made by a self-managed super fund is far greater than with retail and industry superannuation funds. With the SMSF – provided that the dealings are within the confines of the relevant superannuation regulations & the SMSF trust deed – the trustee can invest in a wide range of asset classes. Traditional investments such as shares, term deposits and property trusts are available to the SMSF, plus more unconventional assets like works of art and collectibles.

If the members/trustees of the self-managed super fund have experience and confidence investing in a particular asset class such as residential property, an SMSF will allow them to directly access this asset class where a retail or industry fund will not.

Trustees can also quickly adjust their investment portfolio as and when it suits them – a fast response can be made to any changes in market conditions, superannuation laws or the member’s personal circumstances.

3. Leverage – punching above its weight

Prior to the introduction of borrowing rules in 2007, superannuation funds could not borrow funds to purchase investments. Since 2007, SMSFs can now borrow or leverage to obtain more funds for investment just like investors can outside of the superannuation environment.

The trustees and members of the fund get an opportunity to build their super balances faster due to the extra funds borrowed that allow them acquire assets that would otherwise be out of their reach, such as a direct residential or commercial property. This is also amplified by the fact that self-managed super funds benefit from concessional tax rates – 15% on contributions and earnings.

In the accumulation phase of the SMSF life cycle, any income earned by the fund is only taxed at 15% as opposed to up to 47% for income earned outside of super. In the pension stage of the SMSF, the tax rates are even more attractive. This is down to the fact that there is no tax payable on investment earnings. This includes a 0% capital gains tax rate for assets sold during the pension phase. So that’s 0% tax on earnings, and 0% Capital Gains Tax.

4. Cost – starting and running an SMSF may be cheaper than you think

Despite the type of super fund you choose, there are cost involved, mostly in the form of administration/compliance of the fund, plus investment management costs.

The self-managed fund must file annual tax returns and audits as well as pay fees to the Australian Taxation Office (ATO). These fees are, however, not based on a percentage of the balance of the fund. Retail and industry funds have lower fixed costs than their self-managed counterparts. However, they often charge you in different ways.

Getting deeper into the nitty gritty of the costs associated with self-managed super funds reveals that often a SMSF can be a cheaper alternative to a retail or industry fund. The more that a self-managed super fund grows, the more cost-effective it becomes, but the total cost of running an SMSF will depend on the related investments and any costs associated with engaging professional support.

The costs incurred by a self-managed super fund can still be reduced by the consolidation of the super assets. In an SMSF, you can combine your super assets with up to three other members, creating a larger fund balance but with only one set of fees, rather than four sets of fees.

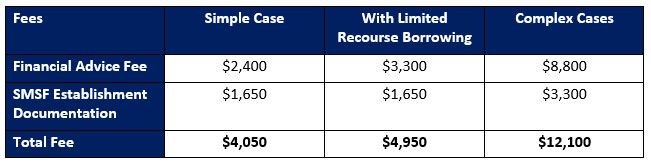

Establishment Costs: Average SMSF Annual Administration & Compliance Fees

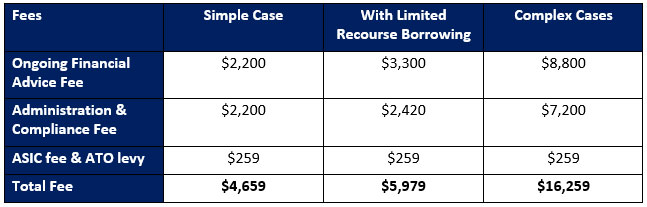

Ongoing Costs: Average SMSF Annual Administration & Compliance Fees

At Assure Wealth, we specialise in helping busy, successful families get their financial house in order, bring structure to their finances and achieve financial peace of mind. We have a particular focus on helping people to establish a self-managed superannuation fund (SMSF), plus self-managed superannuation property investment. Our SMSF service operates on a fee for service basis to offer complete transparency on costs.

Author: Pat Casey – Managing Director, Assure Wealth

Resources

- ASIC Moneysmart’s guide to Self-Managed Superannuation Funds

- The ATO guide to setting up a SMSF

Visit our Financial Knowledge Centre where you will access educational videos and articles, plus join our monthly e-Newsletter to help improve your financial knowledge.

If this article interested you and you would like to speak to Pat Casey on the phone, select a time to speak with Pat Casey – Financial Planner.

At Assure Wealth we specialise in helping busy, successful families structure their finances to achieve peace of mind.

Author: Pat Casey – Managing Director & Financial Planner – Sydney, Assure Wealth

Author: Pat Casey – Managing Director & Financial Planner – Sydney, Assure Wealth

Download the Assure Wealth Corporate Brochure

Disclaimer: The information provided on this website has been provided as general advice only. We have not considered your financial circumstances, needs or objectives and you should seek the assistance of your Walker Lane Pty Ltd Adviser before you make any decision regarding any products mentioned in this communication. Whilst all care has been taken in the preparation of this material, no warranty is given in respect of the information provided and accordingly neither Walker Lane nor its related entities, employees or agents shall be liable on any ground whatsoever with respect to decisions or actions taken as a result of you acting upon such information.

Assure Wealth Pty Ltd ABN 31 965 466 780 Corporate Authorised Representative no. 1244817, Patrick Casey Sub-Authorised Representative no. 1244748 of Walker Lane Pty Ltd ABN 70 626 199 826, an AFSL holder No 509305.