It’s been a wild ride for investors in recent weeks, with daily market volatility at levels not seen since the Global Financial Crisis more than a decade ago.

Heightened market volatility isn’t likely to dissipate anytime soon, fuelled by ongoing coronavirus contagion fears and economic shocks as governments and businesses grapple with containing its spread.

But it’s not good investment sense to be swayed by the day-to-day movements of financial markets, especially by reacting to volatility with knee-jerk investment decisions.

Instead, it’s important to have a long-term investment strategy and diversified asset allocation plan, and not to deviate from that plan, even when markets do fall sharply.

Three mistakes to avoid during a downturn

1. Failing to have a plan

Investing without a plan is an error that invites other errors, such as chasing performance, market-timing, or reacting to market “noise.” Such temptations multiply during downturns, as investors looking to protect their portfolios seek quick fixes.

2. Fixating on losses

Market downturns are normal, and most investors will endure many of them. Unless you sell, the number of shares you own won’t fall during a downturn. In fact, the number will grow if you reinvest your funds’ income and capital gains distributions. And any market recovery should revive your portfolio too.

3. Overreacting or missing an opportunity

In times of falling asset prices, some investors overreact by selling riskier assets and moving to government securities or cash equivalents. But it’s a mistake to sell risky assets amid market volatility in the belief that you’ll know when to move your money back to those assets.

A minimum volatility approach

In a recent article (The investment portfolio X factor), we referred to the growing use of actively managed funds and exchange traded funds designed to deliver market outperformance based around specific investment factors.

And we referred to “minimum volatility” factor funds, which aim to minimise the impact of market volatility on a portfolio by actively filtering out the most volatile companies.

Minimum volatility funds perform best over longer-term periods, and are designed to appeal to investors who desire a less volatile equity return experience.

They aim to reduce risk with a degree of downside market protection while maintaining the ability to participate in the upside potential of the broad equity market.

Used as a portfolio strategy, minimum volatility funds can complement other equity allocations. They target shares that have lower-than-market volatility characteristics but do not deliver lower-than-market returns.

This means a fund can invest across a large group of shares that have demonstrated lower volatility than the market over a period of time and can potentially achieve better long-term risk-adjusted returns than by investing in the broader market.

Share weightings are generally determined through a portfolio optimisation process that seeks to construct the least volatile portfolio on a forward looking basis. The shares distribution is narrower, protecting more on the downside risk, and adding currency hedging to a strategy will also eliminate foreign exchange risk.

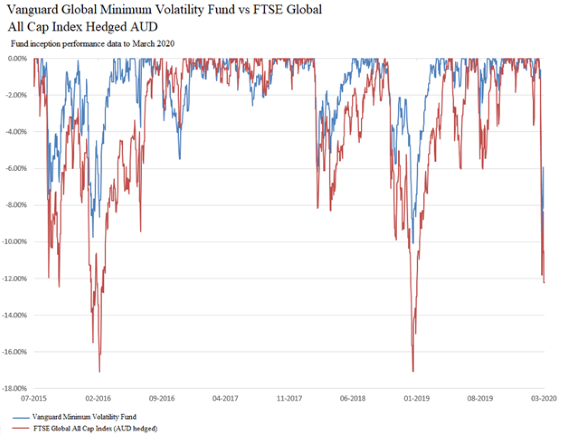

Lowering volatility can pay off

The chart below shows the performance of the Vanguard Global Minimum Volatility Fund (the blue line) versus its benchmark FTSE Global All Cap Index Hedged AUD (the red line). In times of very severe market falls, similar to those we are currently experiencing, the fund has demonstrated much lower volatility against the market index.

On an Australian dollar hedged basis over rolling three-year periods, Vanguard data shows that a minimum volatility approach has achieved 30-40 per cent average reductions in portfolio volatility against the broader market.

Volatility reduction strategies are attractive because they can provide a smoother investment ride than a broader market index.

The growth in funds under management within minimum volatility funds is a sign of proactive interest by investors wanting to use them as a complement to their broader equities markets exposures.

A minimum volatility strategy can help weather volatile markets but, as with any active investment strategy, it’s important to take the time to understand the objectives and be cognisant of the risks, which potentially will include periods of underperformance.

Conclusion

Following these steps can allow you to head into retirement with confidence and the necessary information to design the post-work life you desire.

If this article interested you and you would like to speak to Pat Casey on the phone, select a time to speak Pat – Financial Planner Sydney.

At Assure Wealth we specialise in helping busy, successful families structure their finances to achieve greater wealth and financial peace of mind.

Author: Pat Casey – Managing Director & Financial Planner Sydney – Assure Wealth

Download the Assure Wealth Corporate Brochure

Disclaimer: The information provided on this website has been provided as general advice only. We have not considered your financial circumstances, needs or objectives and you should seek the assistance of your Walker Lane Pty Ltd Adviser before you make any decision regarding any products mentioned in this communication. Whilst all care has been taken in the preparation of this material, no warranty is given in respect of the information provided and accordingly neither Walker Lane nor its related entities, employees or agents shall be liable on any ground whatsoever with respect to decisions or actions taken as a result of you acting upon such information.

Assure Wealth Pty Ltd ABN 31 965 466 780 Corporate Authorised Representative no. 1244817, Patrick Casey Sub-Authorised Representative no. 1244748 of Walker Lane Pty Ltd ABN 70 626 199 826, an AFSL holder No 509305.