Considering that I’m a Sydney-based Financial Planner in my 30s this is a question that I often hear, and feel somewhat qualified to answer. Most of my friends, and parents at my daughter’s school, are between the ages of 35 and 45, and one thing I have noticed is that there is a general misunderstanding of what it is that I actually do for clients on a day-to-day basis.

My answer to the question is as follows:

“I help you get your financial house in order, to help maximise the chance of you achieving your financial goals faster, easier, and with more certainty than you could achieve yourself”.

This is a very general answer to a very general question. However, the advice that I end up delivering to each couple is different because everyone’s personal circumstances are different. In saying that, the key areas of financial advice are always the same:

We Ask You Lots of Questions to Understand Your Current Position

When I first meet with someone, there are two main aims of the initial conversation:

- Do I believe that I am the right person to help them?

- Do they believe that I am the right person to help them?

To answer these questions, I first need to understand what current problem or challenge they are looking to address. Often, it’s hard to articulate a specific problem, and the challenges can be even more general in nature:

- “I just feel like we’re getting nowhere financially and we need help”

- “I think that we could be doing more with our finances, but I don’t know where to start”

- “We both want to get ahead financially and we’ve decided now’s a good time to start”

Creating an accurate picture of your current situation in terms of personal, family, and financial positions is very important, and involves examining:

| Children | Working status | The family balance sheet – assets and liabilities | Family trusts or business structures |

| Do you have multiple super funds? | Household income | Your superannuation funds | Are you in an occupation that is at risk of being sued? |

| Your mortgage | Plans to change employment status | Where your superannuation is invested | Current Estate planning – Wills, POAs etc |

| Personal debts – car, credit card etc | Plans to renovate your house | Do you have any personal or health insurance? | Income and expenditure |

We Help You Paint a Picture of Your Ideal Future Position

Describing what a better future looks like can be very difficult. We become so accustomed to the status quo that sometimes it’s hard to break free and think about what else is possible.

Do you dream about paying off the mortgage faster? Retiring early? Starting a business? Leaving your corporate job? Moving to part-time work? Buying an investment property? Taking 6 months off to take the family to Europe? Or, just achieving financial peace of mind, knowing that if anything unfortunate was to happen to you or your partner your family wouldn’t have to worry about money?

This is what a Financial Planner helps draw to the surface.

Developing a Timeframe to Achieve Your Goals

Failing to plan is planning to fail. Therefore, putting some rough timeframes around achieving your ideal future financial position is important to motivate you not only to take action, but also to stay disciplined throughout the journey.

Plans change over time as people change. There’s nothing wrong with that. By taking action and improving your financial position, you open up opportunities that weren’t previously available to you. Sometimes, this causes people to tweak or revise their goals once they learn what’s truly important to them.

Personally, I start with asking people to describe their ideal position in 10 years’ time.

Here’s a tip: Females seem to be far better at this than men.

I don’t know why that is so, but, as a man, I do know I find it difficult to project my mind that far into the future. However, having done it myself, I also know and understand why it’s so important. In our 30s and 40s, we tend to overestimate what we can achieve in the next year, but we tend to underestimate what we can achieve in the next 10 years.

Let’s face it, 10-year goals are a long way away. I find bringing it back to 3-year goals makes them more ‘real’ and gives you more motivation to take action today. Short-term goals then help you determine what actions need to be taken right NOW.

What Actions Need to be Taken Right NOW

For couples in their 30s and 40s, the most common action items that I’ve identified are:

1. Estate Planning Review

- a. Who do you want to look after your children if both of you pass away?

- b. How will their living expenses be funded?

- c. How can this be funded in the most tax effective way?

- d. If your children are under 18, how can your assets be protected?

- e. How do you want your assets to be distributed, and to whom?

- f. Who do you wish to nominate as the Executor of your Will?

- g. Who do you want to nominate to look after your financial and medical affairs if you’re unable to yourself?

- h. Which Estate Planning Specialist do you want to engage to draft your plan?

- i. How is your estate plan to be funded?

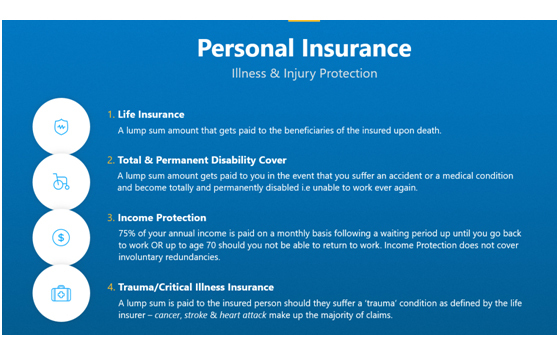

2. Personal Insurance Review

- a. What types of insurance do you need?

- b. How much insurance do you need?

- c. How do you structure your insurance premiums to maximise affordability, and minimise the impact on your cash flow?

- d. How do you take advantage of tax deductions?

- e. Does someone who’s not working need insurance?

Source: www.assurewealth.com.au

3. Wealth Creation Review

- a. Conducting a review on your current superannuation and investments.

- b. Identifying how much investment risk you are currently taking.

- c. Identifying how much investment risk you should be taking to meet your future goals.

- d. Is your superannuation structured appropriately to meet your goals?

- e. Are the fees you are paying too high?

- f. Where is the best place to invest your money – shares, property, cash, term deposits etc?

- g. Would you consider borrowing to invest?

- h. Is a Self-Managed Superannuation Fund (SMSF) an option?

4. Asset Protection Review

- a. What is the current ownership structure of your family home?

- b. Are either of you in a high-risk occupation/business?

- c. How is your business currently structured?

- d. Do you have an existing family trust?

- e. Do you have a Self-Managed Superannuation Fund (SMSF)?

- f. Do you need to engage an Asset Protection Specialist to structure your affairs differently to protect your assets?

5. Cash Flow Review

- a. Income and expenses review.

- b. Identifying excess cash flow or shortfall.

- c. Debt consolidation review.

- d. Debt reduction review.

- e. Identifying options to invest excess cash flow.

Source: www.assurewealth.com.au

Did you notice that there’s nothing about what shares to buy, sell, or hold?

Also, there’s very little mention of tax.

That’s the role of a Stockbroker and an Accountant respectively. A Financial Planner takes a much more holistic view of your situation, and then calls in the subject matter experts where necessary.

In your 30s and 40s, to build your ‘A’ team of professionals, I recommend engaging with the following specialists:

- Start with a Financial Planner to look at your entire financial position

- A great Accountant to address your tax affairs

- An investment savvy Mortgage Broker to ensure that your debt is structured correctly for your cash flow and debt reduction

- An Estate Planning Lawyer to draft your Wills, Powers of Attorney, Enduring Guardianship, and Testamentary Trusts

- An Asset Protection Lawyer if you are self-employed, in a business partnership, or in a high-risk occupation where there’s even the slightest chance you may be sued and your personal assets may be at risk

You may be asking yourself where you can find these professionals – ones who are great at their profession, not duds. For a Financial Planner or Accountant, start with recommendations from friends. Once you have engaged these professionals, you will generally find they have conducted their own due diligence and can recommend a panel of high quality Mortgage Brokers and Lawyers to their existing clients.

In summary, hopefully this article has opened your eyes on what a Financial Planner actually does for people in their 30s and 40s.

After new clients have gone through the process with me, they often comment that, originally, they were unsure if they needed a Financial Planner, or if a Financial Planner would want them as a client because they didn’t have a million dollars to invest. After the process, their financial affairs are structured correctly in a tax efficient manner, they accelerate their wealth accumulation, have risk mitigation and estate plans in place, and feel far more comfortable, happy and confident.

Source: www.assurewealth.com.au

If this article interested you and you would like to speak to Pat Casey on the phone, select a time to speak Pat – Financial Planner Sydney.

At Assure Wealth we specialise in helping busy, successful families structure their finances to achieve greater wealth and financial peace of mind.

Author: Pat Casey – Managing Director & Financial Planner Sydney – Assure Wealth

Author: Pat Casey – Managing Director & Financial Planner Sydney – Assure Wealth

Download the Assure Wealth Corporate Brochure

Disclaimer: The information provided on this website has been provided as general advice only. We have not considered your financial circumstances, needs or objectives and you should seek the assistance of your Walker Lane Pty Ltd Adviser before you make any decision regarding any products mentioned in this communication. Whilst all care has been taken in the preparation of this material, no warranty is given in respect of the information provided and accordingly neither Walker Lane nor its related entities, employees or agents shall be liable on any ground whatsoever with respect to decisions or actions taken as a result of you acting upon such information.

Assure Wealth Pty Ltd ABN 31 965 466 780 Corporate Authorised Representative no. 1244817, Patrick Casey Sub-Authorised Representative no. 1244748 of Walker Lane Pty Ltd ABN 70 626 199 826, an AFSL holder No 509305.