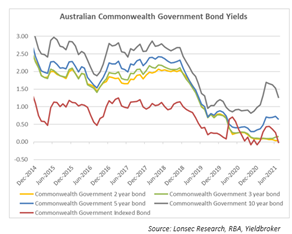

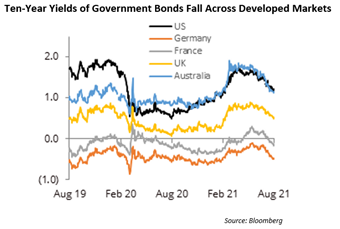

According to a report in Bloomberg recently, while Vanguard data show a portfolio with 60 equities/fixed income mix returned an average 9.1% a year from 1926 to 2020, JP Morgan Asset Management recently estimated it will return just 3.7% over the next decade. Why? In a world where 85% of developed-market government bonds are yielding below 1%, the likely returns from the fixed income component of the portfolio has plunged, as shown in Figures 1 and 2.

So, this raises a question that we are getting asked by our clients – why even bother having fixed income within my portfolio?

When answering this question, it is important to think about what the reasons were for including fixed income in your portfolio in the first place.

At Lonsec, we believe that fixed income generally can play three roles in a portfolio:

- As a diversifier to equities – bonds dampen overall portfolio volatility when held in a portfolio with riskier assets such as equities;

- As a defensive asset that “will not go down” – so may be suitable for the risk averse investor with a primary objective being the preservation of capital; and

- As a provider of a steady income stream – regular income payments from bonds provide a stable income stream for retirees

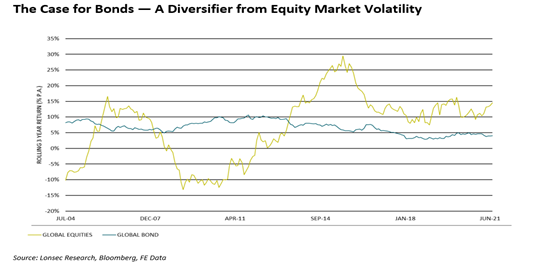

Figure 3 shows the rolling three year returns for global equities and global bonds and serves to highlight the relatively low volatility of global bonds compared to global equities.

However, when faced with the prospect of challenging returns, the reasons for inclusion tend to fall by the wayside and we start to focus on where to find better returns. As a result, we have seen many investors move out of fixed interest securities, especially longer term government bonds, in favour of equities or a taking a bar bell approach by investing in the extremes of lower quality investment grade bonds and short duration cash like securities. This is a dangerous proposition especially for those in retirement.

Becoming a victim of short-termism and negative momentum can shift your portfolio greatly to one that effectively eradicates each of those objectives we listed above. Why?

- When we increase our allocation to equities or riskier assets, we are reducing our diversification. This will significantly increase the volatility of the portfolio.

- Whilst the short duration assets will act has a buffer during times of market volatility, we have seen time and time again, that lower quality investment bonds will typically have their correlation to equities rise to 1 during periods of market stress and produce a very significant negative return that effectively wipes out any ‘buffering’ that the short duration assets may have provided.

- During periods of economic stress, the stability of income from equities can change quickly. We saw this last year when many banks cut their dividends for a short period of time to ensure their books were able to withstand the changing economic landscape.

- For retirees, unless the income provided through dividends and higher yielding fixed income securities is sufficient enough to live on, the impact of falling markets when in drawdown can be catastrophic to the long term viability of a retirement portfolio.

The question around the validity of longer duration bonds in portfolios is a valid one. Fund managers have been able to lean on these as performance enhancers as dovish central banks have overseen 20 years of falling interest rates. This, coupled with the relentless demand for safe haven assets from investors, especially during times of equity market stress, has seen abnormally high returns being achieved in this end of the market.

A fact that we all quickly forget about volatility is that with riskier assets not only do you have a greater probability of producing higher returns, you also have a greater probability of producing lower returns.

Whilst historically it has been easy to forget about fixed interest as the asset class has taken a backseat to the action packed excitement of the sharemarket, we cannot do this anymore, especially if you are approaching or in retirement. This is the stage where preservation of capital with a guaranteed income stream becomes the most important goal.

For those especially, bond investors now have three choices:

- Take on more risk to generate higher yields;

- Lower return expectations for the short to medium term; or

- Accept low rates as something they cannot change.

If you would like assistance getting your accounts under control as we approach the end of financial year, call us today on 1300 79 80 38.

Visit our Financial Knowledge Centre where you will access educational videos and articles, plus join our monthly e-Newsletter to help improve your financial knowledge.

If this article interested you and you would like to speak to Pat Casey on the phone, select a time to speak Pat – Financial Planner Sydney.

At Assure Wealth we specialise in helping busy, successful families structure their finances to achieve greater wealth and financial peace of mind.

Author: Pat Casey – Managing Director & Financial Planner Sydney – Assure Wealth

Download the Assure Wealth Corporate Brochure

Disclaimer: The information provided on this website has been provided as general advice only. We have not considered your financial circumstances, needs or objectives and you should seek the assistance of your Walker Lane Pty Ltd Adviser before you make any decision regarding any products mentioned in this communication. Whilst all care has been taken in the preparation of this material, no warranty is given in respect of the information provided and accordingly neither Walker Lane nor its related entities, employees or agents shall be liable on any ground whatsoever with respect to decisions or actions taken as a result of you acting upon such information.

Assure Wealth Pty Ltd ABN 31 965 466 780 Corporate Authorised Representative no. 1244817, Patrick Casey Sub-Authorised Representative no. 1244748 of Walker Lane Pty Ltd ABN 70 626 199 826, an AFSL holder No 509305.