HOW TO BUY PROPERTY USING AN SMSF – PART 2 – THE PROCESS

In part 1 we investigated the background for SMSF loans or Limited Recourse Borrowing Arrangements (LRBAs), which facilitate SMSF’s borrowing money to invest in property.It’s now time to look at the nuts and bolts of how it’s done. (please note: This section refers to the rules in place in New South Wales; rules do vary slightly between different states and territories)

With SMSF Property investment, following the correct process is extremely important. Certain steps must be taken before others, especially if you are at the stage where you want to put an offer on a property.

Borrowing via a LRBA can seem daunting, but if you follow the process carefully, and plan well in advance, it becomes easier to understand.

The most important requirement is that you, or those acting for you, are fully aware of the borrowing exceptions permitted by section 67A of the Superannuation Industry Supervision (SIS) Act.

Now, let’s look at the process, step by step:

1. The loan can only be used for the acquisition of “a single acquirable asset”. This can include a residential or commercial property. However, if a unit and a car space are on separate titles, this may not meet the requirements as it isn’t a ‘single’ asset. If in doubt, seek legal advice as this is very important.

2. The asset purchased must be kept in trust by a second Trustee called the “the Custody Trust” or the “Bare Trust” whilst there is a loan in place. Do not purchase the property in the name of the SMSF Trustee, and definitely don’t pay the deposit from your personal funds. Seek advice from a professional around the correct entity to purchase the property in.

3. The SMSF Trustee has the right to gain legal ownership of the asset once the loan is fully repaid. Until such a time, ownership remains with the Custody/Bare Trust.

4. If there is a default on the loan (i.e missed repayments), the lender can only claim against the ‘single acquirable asset’ and not against any other assets which form part of the SMSF such as your cash account, managed funds or shares. Be careful, some lenders will ask you to sign a personal guarantee which may put your personal assets at risk. Your lender will most likely include a requirement to have a Lawyer explain and witness your signatures on your personal guarantee.

5. The loan can only be used to purchase assets that the SMSF would be permitted to purchase if it was using its own funds. That means you still need to meet the ‘sole purpose test’ and you can’t go invest in a new boat to use on the weekends……..

If you fulfill these criteria, and you believe that property investment and this borrowing strategy are appropriate for your SMSF, you should proceed in the following manner:

THE PROCESS

1. Have your Financial Adviser gather the data for your superannuation balances, including evidence of the contributions you have made for the previous three years and what you expect to make in the future.

2. Take these figures to your Mortgage Broker and ask for an assessment of whether;

• you are likely to be eligible for a SMSF loan

• how much you can borrow, and

• the maximum amount that you can borrow to maintain a cash buffer, plus pay for expenses such as stamp duty

• Finally, the maximum amount you can spend on a property i.e your limit

This is a very important step, because without lender agreement,time and money spent on other parts of the process may end up wasted.

3. With your Financial Adviser, commence the process of setting up your SMSF (if you don’t have one already). This will require your Adviser to undertake a detailed data collection process, including getting a good understanding of your personal and financial goals.

4. If a SMSF is appropriate for your needs, your Financial Adviser will make a recommendation via a Statement of Advice to set up a SMSF and facilitate the set-up process with you including;

• Set up the Trustee company

• Drafting the Trust Deed

• Drafting the investment strategy and the investment goals of the fund

• Considering the insurance needs of the members of the fund

• Set up the Custody/Bare Trust with a Corporate Trustee

• Engaging an Accountant to facilitate the ongoing administration of the fund, plus an Auditor to conduct the annual audit of the SMSF

5. Your SMSF Trust Deed must allow the fund to borrow and allow a bare trust/custodian trust to hold an asset (i.e a residential or commercial property) for the SMSF Trustee.

6. Your fund’s investment strategy should reflect that the Trustees have considered the risks involved in the desired investment and have adopted strategies to minimise risks (i.e insurance) as well as cash buffers and additional future super contributions. Always allow for unexpected vacancies where no rent is collected.

7. Only now are you in a position to start looking at properties to buy.

8. Find the property you want to buy and open negotiations with the seller. At the same time give your Mortgage Broker the details of the property so they can have it valued and confirm they are able to secure you the loan via the lender.

9. Agree on a final price for the property with the seller and exchange contracts. Avoid using any personal funds for the deposit.

10. The purchaser on the sale contract is the Corporate Trustee of the Custodian/Holding/Bare Trust. I cannot stress how important this is to get right.

11. Finalise your loan agreement and terms with your Mortgage Broker.

12. Sign the trust deed of the Holding Trust as SMSF Trustee and have the Bare/Custodian/Holding Trustee do the same.

13. Have the borrower (that is, the SMSF Trustee) sign the loan and mortgage agreements with the lender.

14. Finalise the necessary payments to settle the purchase. These should come from the lender directly to the seller.

15. Pay stamp duty from the SMSF bank account (not your personal funds). Seek advice on how to dcument this based on the state where you are purchasing to avoid double stamp duty in the future.

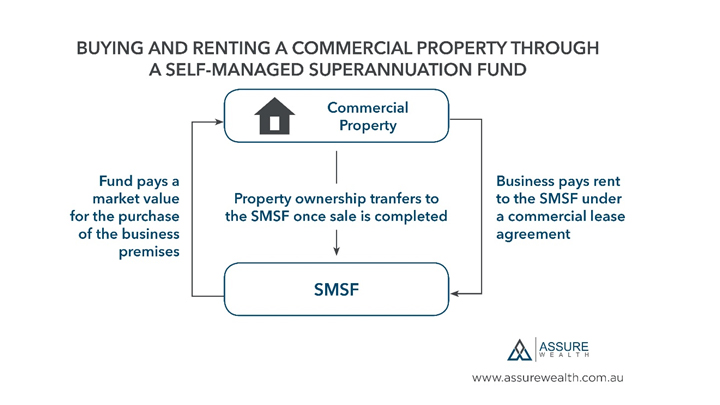

16. If you are purchasing a commercial property to operate your business from, set up a tenancy agreement with the Holding Trust Trustee being the name on the lease. You can find templates to purchase via various Law Firm’s websites.

17. The best place for the rental income to go is to the bank account of the SMSF Trustee. It is not advisable for the Holding Trustee to open a bank account for this purpose, nor to apply for a tax file number.

18. The loan payments are set up to be paid from the SMSF Trustee to the lender.

19. If applicable, the SMSF trustee should register for land tax (depending on what state you are in the rules vary, therefore legal advice should be sought).

20. Seek advice from your Accountant/Tax Agent on whether you should register the SMSF for gst. In the event you are purchasing a commercial property, it’s common to register the SMSF for gst.

21. When the loan is fully paid off, the property should be transferred from the Holding Trustee to the SMSF Trustee. As long as the Holding Trust deed is stamped to prove previous payment of Stamp Duty, only a nominal sum should be due to transfer the asset. Seek advice at this point.

As you can see, the process is not exactly simple, but it need not be too difficult provided you proceed with care,complete each step, and, most importantly, make sure that you get the advice of an experienced SMSF specialist Financial Planner at every stage.

Do not attempt to undertake this whole process on your own as every purchase has its own challenges and the rules are different for every state. A small investment in good advice now could save you an enormous bill in the future.

To investigate this topic further, watch this video.

(Note: Each state and territory in Australia has slightly different rules but these guidelines will ensure you remain within regulations)

https://www.moneysmart.gov.au/superannuation-and-retirement/self-managed-super-fund-smsf

At Assure Wealth, we specialise in helping busy, successful people to get their financial house in order, bring structure to their finances, and achieve financial peace of mind. We focus on helping clients establish self-managed superannuation funds (SMSF), and self-managed superannuation property investment portfolios. We charge on a fee for service basis to offer complete transparency on our fees.

Visit our Financial Knowledge Centre where you will access educational videos and articles, plus join our monthly e-Newsletter to help improve your financial knowledge.

If this article interested you and you would like to speak to Pat Casey on the phone, or meet at either our Sydney CBD or Southern Sydney offices, select a time to speak with Pat Casey – Financial Planner.

Author: Pat Casey – Managing Director & Financial Planner – Sydney, Assure Wealth

Author: Pat Casey – Managing Director & Financial Planner – Sydney, Assure Wealth

To find out more, visit us at: www.assurewealth.com.au

Disclaimer: The information provided on this website has been provided as general advice only. Assure Wealth does not provide direct property advice. We have not considered your financial circumstances, needs or objectives and you should seek the assistance of your Walker Lane Pty Ltd Adviser before you make any decision regarding any products mentioned in this communication. Whilst all care has been taken in the preparation of this material, no warranty is given in respect of the information provided and accordingly neither Walker Lane nor its related entities, employees or agents shall be liable on any ground whatsoever with respect to decisions or actions taken as a result of you acting upon such information.

Assure Wealth Pty Ltd ABN 31 965 466 780 Corporate Authorised Representative no. 1244817, Patrick Casey Sub-Authorised Representative no. 1244748 of Walker Lane Pty Ltd ABN 70 626 199 826, an AFSL holder No 509305.