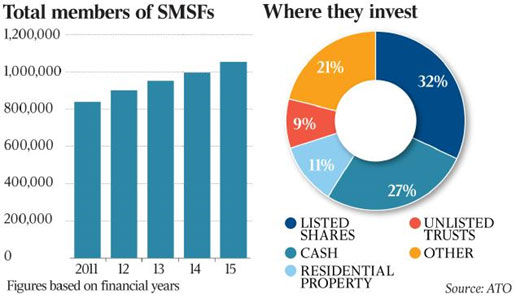

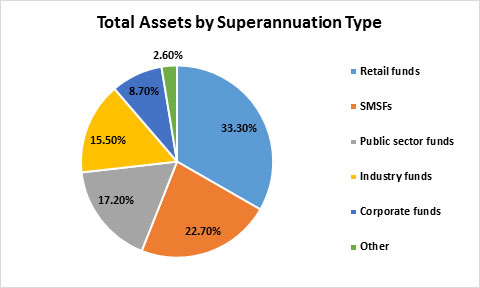

Many Australians are now looking to take control and become more involved in their superannuation. SMSFs hold approximately one-third of the total superannuation funds, and are often the preferred choice for people who are highly engaged with their superannuation and retirement planning.

Many Australians are now looking to take control and become more involved in their superannuation. SMSFs hold approximately one-third of the total superannuation funds, and are often the preferred choice for people who are highly engaged with their superannuation and retirement planning.

Let’s start looking at some of the benefits of an SMSF.

1. Investment Choice

One of the key benefits of a SMSF is investment control, and the wider investment choices such as residential and commercial property, collectibles, term deposits and direct shares that SMSF members have compared to industry and retail super funds. You will also have access to derivatives to offer downside protection or hedging your portfolio risk.

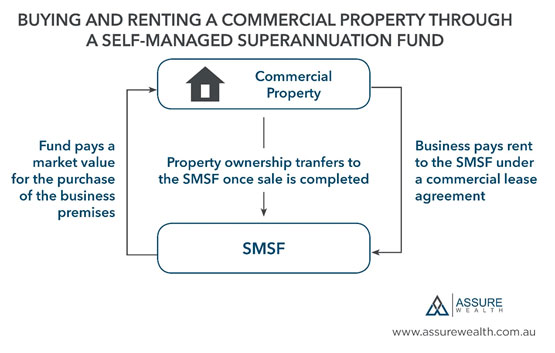

One of the main reasons that SMSFs are recommended for small business owners is to be able to have business property owned by their SMSFs and then leased back to the business. This gives a steady income for SMSFs and frees up any capital in order to grow your business and provide secure tenancy.

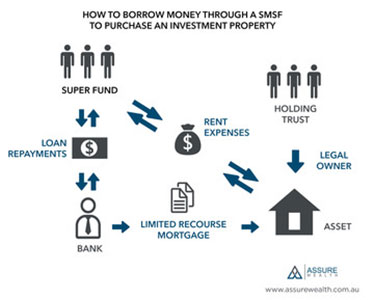

2. A SMSF can borrow to invest in property

With the rules that allow SMSFs to borrow, SMSF members can now purchase large single assets such as commercial property that would otherwise be outside of their reach. For example, a couple with a combined SMSF balance of $200,000 can borrow money via a limited recourse loan to purchase an investment property worth $400,000. Generally, a limited recourse loan can be secured for up to 60%-70% of the purchase price of a property. This excludes other costs associated with the purchase such as legal, stamp duty etc.

Important rules to note:

- Residential investment properties purchased through an SMSF cannot be lived in by you, any other trustee or anyone related to the trustees.

- Don’t buy a “renovator’s dream”. Borrowed funds can be used for property maintenance but cannot be used to improve a property. This also means that you cannot buy and empty block of land with the view to build a property on it at a later stage. This also means that you can’t purchase a development site with the view to develop it at a later date, or buying an old house with the plan to knock-down rebuild.

SMSF property borrowing risks include:

- Higher costs than a normal home loan – SMSF property loans are more expensive than other property loans. On average, you can expect to pay an interest rate that is approximately 2% higher than a standard investment property loan.

- Cash flow – Debt repayments must be made from your SMSF which means your fund must always have sufficient cash flow to meet the loan repayments. This is the reason many SMSF investors choose high cash flow properties such as commercial property because the rent collected often exceeds the loan repayments.

- Hard to exit – Unwinding the arrangement or selling the property may cause substantial costs to the SMSF. Buying a property through a SMSF should be seen as a long-term investment – at least 10 years if not more. Any less and the transaction costs will eat away any potential benefits.

- Reduction in negative gearing benefits – Any tax and depreciation losses from the property cannot be offset against your taxable income outside of the SMSF.

- No alterations to the property – Until the SMSF property loan is 100% paid off, alterations or improvements to a property cannot be made if they change the ‘character of the property’.

3. Tax Minimisation

Apart from defined benefit super funds (like a government employee fund), most other superannuation funds will offer the ability to take a tax-free pension as an income stream upon retirement.

Another benefit of an SMSF is that it gives you more flexibility than any other superannuation structure when it comes to contributions, the timing of contributions, allocating earnings to particular members and implementing ‘reserves’.

This provides trustees and their professional advisers the ability to use the unique flexibility of an SMSF to minimize the amount of overall tax that the SMSF members pay within the fund, by taking their unique situation into consideration and making strategic decisions on contributions, reserves and distributions. In a public offer or ‘pooled’ superannuation fund, your unique circumstances cannot be considered because you are just one of thousands or even millions of members who all must be treated the same. This means that the trustee of the large superannuation fund may make a decision that negatively affects your tax position, and you have no way to prevent this.

4. Tax Control

Through timing pensions and structuring as well as tilting investment strategies to utilise the concessional tax treatment for the funds, like targeting franking credits, tax can be reduced and for most retirement phase client’s refunds can be claimed from ATO for any excess credits.

There is also the flexibility when it comes to dealing with taxable liabilities for your fund, as this fund only has one single tax return although there may be up to four different members for the fund and each can have numerous pension accounts. Where the fund has one or more members who have retired and are therefore paying 0% tax, tax advantages can be achieved by allocating earnings from members who are not retired and are therefore sitting in a 15% tax environment.

5. Pay for your Life Insurance through your SMSF

You are able to pay for your personal insurance cover through a SMSF. This includes;

- Life Insurance

- Total and Permanent Disability (TPD) Insurance, and

- Income Protection insurance

You may have some insurance cover through your current industry or retail fund. This cover is referred to as ‘group insurance’ and isn’t tailored towards your needs, plus it can be reduced or cancelled by your super fund at any time without your consent.

If you apply for personal insurance that is tailored to your individual needs it is ‘guaranteed renewable’. A ‘guaranteed renewable’ policy is an insurance policy feature that obligates the insurer to continue coverage as long as premiums are paid on the policy.

The group insurance cover that you are automatically provided with through your industry or retail fund is often inadequate in terms of the levels of cover, plus the terms and conditions of the insurance contract.

Your insurance needs are highly personal. Your levels of cover should be determined by your age, family structure, income, cash flow requirements, debt levels, assets and liabilities to name a few variables.

Only a qualified Financial Planner can make a full assessment of your personal insurance requirements, plus make a recommendation on the following;

- What insurance cover you require – life, TPD, IP etc

- The levels of insurance cover

- The best premium structure for your situation

- Options and add-on’s to your policy that are relevant to you

- Which insurance company offers the contract that is best for you, based on the quality of the cover and the premiums. Like with anything in life, often the cheapest option isn’t the best option.

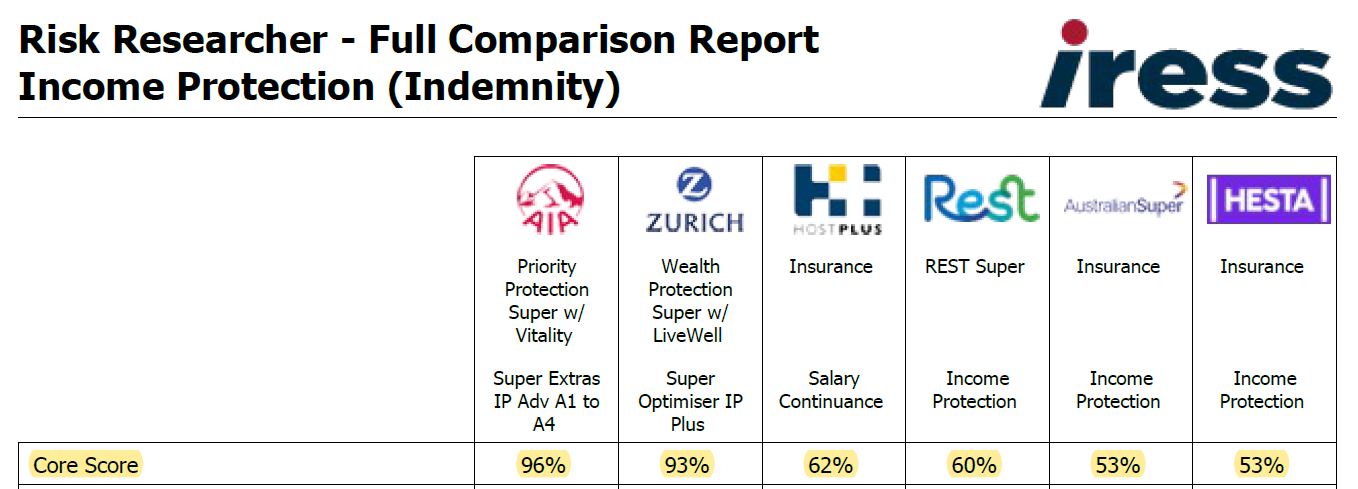

Example: Comparison of Insurance Contract Ratings

Below you can see the comparison of two personal, retail insurance policies for a male in a white collar role (AIA and Zurich with three group insurance policies via industry funds – HostPlus, Rest and Hesta).

Highlighted is the ‘core score’ which is a score out of 100 which measure the quality of the insurance contract. The closer the score is to 100, the higher the quality of the contract. Low scores indicate the contract is of poor quality and is likely to be harder to make a claim on the policy.

Important – this example is for illustration purposes only and will vary from person to person.

6. Minimise transaction costs: brokerage, buy/sell, and CGT spread costs:

Whenever it comes time to move to the pension/retirement phase an SMSF will allow you to have an almost seamless transition from the accumulation phase to the pension phase without the need to sell down assets, therefore not triggering capital gains tax (CGT) and other transaction costs. You do not need to sell your assets such as shares which would incur various taxes and fees in the process. You just retain your investments and begin to draw down on your SMSF balance as an income.

With many industry and retail funds, when moving from Accumulation phase (when you are working) to Pension phase (retirement) you will be forced to sell down your super fund assets when leaving the accumulation phase, then re-purchase new assets within the Pension phase.

Whenever assets are sold or purchased there are transaction costs such as brokerage, buy/sell costs and Capital Gains Tax. A SMSF can help reduce these costs.

7. Transferring your wealth to the next generation

There are plenty of useful estate planning benefits that are built into Australia’s superannuation system. However, an SMSF offers even more benefits, control and flexibility over a member’s estate plan that can ensure that the funds from the SMSF go to the right people, at the right time, in the most tax effective way possible.

Firstly, you will need to be clear that your Will doesn’t control your superannuation benefits unless you nominate for your superannuation balance to form part of your estate.

Keeping superannuation assets outside of the Will may be a smart move, especially considering if you have a blended family, plus the high rate of success when people formally challenge a Will who feel that they have been unfairly treated. With an SMSF, you are able to create a strategy that will execute your wishes for distributing your wealth, with superior tax outcomes. This includes being able to leave your taxable pensions to dependents who are able to receive them tax free, or substantially tax free for non-dependents.

You are also able to structure tax-effective income streams to your dependents like disabled children, or a sick spouse with control around when they receive the pension income and any the lump sum. A simple example of this is that you may nominate to pay a dependent child an income of $60,000 a year for 10 years, rather than a lump sum of $600,000 immediately upon your death. Another option would be to pay $120,000 upfront to fund large upfront expenses, then pay the remaining balance evenly over the next 10 years. This strategy is very powerful when the dependents are young children who are not in a position to manage their own money, or where there are spendthrift beneficiaries – e.g problem gamblers.

8. Asset Protection

Asset protection can be a key consideration for many people, especially business owners and superannuation can be a structure that protects the members from litigation and bankruptcy. In either of these events, your superannuation benefits are likely to be protected from creditors. In the event of a failing business venture, a business owner may be left with their superannuation balance as their only remaining asset. However, as superannuation is intended for retirement, your superannuation balance cannot be used to prop up a struggling business.

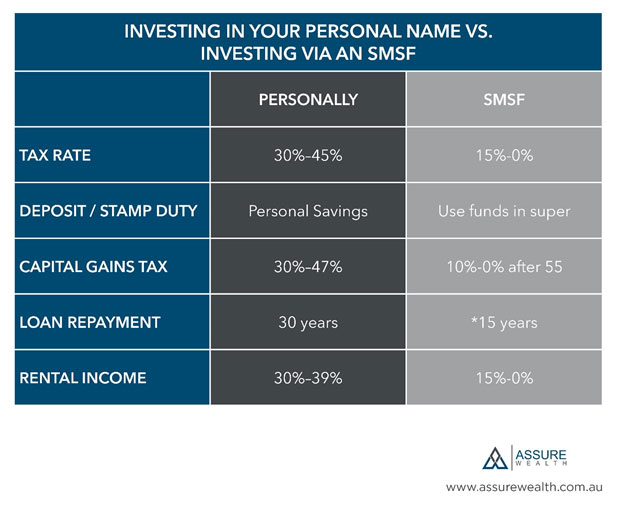

For example, if asset protection is your main goal you would be better placed purchasing an investment property within a SMSF, as opposed to purchasing the property in your own personal name.

9. Cost Savings for higher balances

For some people, the cost of having an SMSF can be lower than alternative public offer super funds, especially when the fund balance is high – greater than $300,000.

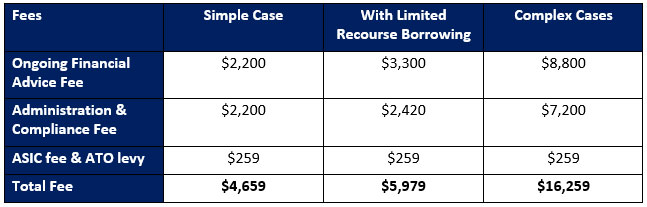

The cost of SMSF annual administration is around $2,000 to $3,000 p.a which includes audit and accounting fees. Retail super funds charge approximately 1.5%, which is $3,000 p.a on an account balance of $200,000.

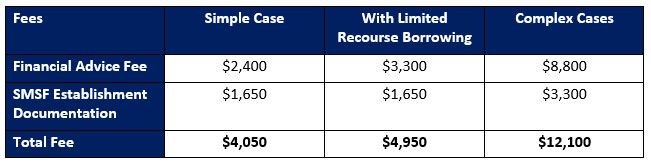

Example of Establishment Costs: SMSF Annual Administration & Compliance Fees

Example of Ongoing Costs: SMSF Annual Administration & Compliance Fees

There has been a clear trend for the last few years that more and more Gen X’s, or those born between 1965 and 1980 are starting their own SMSFs as they have managed to have superannuation for most of their working lives and have now managed to accumulate approximately $200,000 in their superannuation account (or combined with their partner). Contrary to popular opinion, it’s not necessary that these people believe that they can achieve superior performance by making their own investment decisions, however it’s more to do with the fact that they would prefer to have full control, flexibility and transparency over their own money.

There are many benefits that will make self-managed superannuation a very attractive option for many people as opposed to traditional industry or retail super funds.

Author: Pat Casey – Managing Director & Financial Planner Sydney – Assure Wealth

Where to from here?

Look to team up with professionals that have experience in the strategies that will suit your needs. An SMSF will allow you to have ultimate control over selecting your team of professionals, and how you will pay for their advice. There may be the opportunity to pay for their fees via your SMSF funds.

Only a qualified Financial Planner can recommend that you establish an SMSF. In the past Accountants could make such a recommendation, however this exemption has now ceased.

Accountants still play a critical role in generating the tax return for the SMSF, however they cannot make any recommendations relating to the set-up, or investments of the SMSF. Therefore, the first professional that you should seek to engage if you are considering starting your own SMSF is a Financial Planner. However, be careful as not all Financial Planners are accredited to provide advice on SMSFs due to their complexity and specialist nature.

In conclusion, Self-Managed Super Funds are popular today and have become the most powerful retirement savings structure available. You must be willing to take on the responsibilities of an SMSF trustee, and a good Financial Planner will help guide you and educate you along the way. You will be able to ‘pass the sleep test’ knowing that you have control of your superannuation, that you control your investment decisions, have maximised your tax effectiveness, and have implemented effective estate planning and asset protection strategies.

If you would like to access more articles and videos, please visit the resources section of our website.

Discover the top 10 reasons

to manage your own super

If this article interested you and you would like to speak to Pat Casey on the phone, select a time to speak Pat – Financial Planner Sydney.

At Assure Wealth we specialise in helping busy, successful families structure their finances to achieve greater wealth and financial peace of mind.

Author: Pat Casey – Managing Director & Financial Planner Sydney – Assure Wealth

Download the Assure Wealth Corporate Brochure

Disclaimer: The information provided on this website has been provided as general advice only. We have not considered your financial circumstances, needs or objectives and you should seek the assistance of your Walker Lane Pty Ltd Adviser before you make any decision regarding any products mentioned in this communication. Whilst all care has been taken in the preparation of this material, no warranty is given in respect of the information provided and accordingly neither Walker Lane nor its related entities, employees or agents shall be liable on any ground whatsoever with respect to decisions or actions taken as a result of you acting upon such information.

Assure Wealth Pty Ltd ABN 31 965 466 780 Corporate Authorised Representative no. 1244817, Patrick Casey Sub-Authorised Representative no. 1244748 of Walker Lane Pty Ltd ABN 70 626 199 826, an AFSL holder No 509305.